In previous articles, the discussion was about the Letter of Intent (LOI). Today’s article will overview the major trend of M&A deals in Japan in 2022 through several publications. Referring to the above, below are the transition of numbers and prices of M&A transactions involving Japanese companies in the recent three years. (All the data bellow is based on RECOF research)

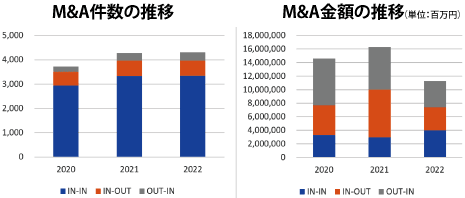

In 2022, there were 4,303 M&A transactions involving Japanese companies and which increased by 0.6% compared to 2021, and a record for two conservatives years. In 2020, due to COVID-19, the numbers of transaction decreased drastically. However, considering that these numbers and prices had been increasing for eight consecutive years from 2012 to 2019, it is reasonable to assume that it has always been an uptrend except for the pandemic year of 2020.

Regarding the number of transactions, “IN-IN” comprises 80% of the overall M&A deals among Japanese companies. On the other hand, although the cross-border deals are only accounted for 20%, this result actually matched the past trend. (Cross-border deals stands for “IN-OUT”, which means M&A deals of foreign companies done by Japanese companies, and “OUT-IN”, which means M&A deals of Japanese companies done by foreign companies).

In addition, financial & non-manufacturing industries also increased their transactions, and the non-manufacturing sector, primarily on the sellers’ side, conducted more than 60% of the transactions. Moreover, as in 2021, transactions in IT fields were promoting DX and transactions for sustainability-related businesses, which are environmentally friendly and popular.

While the number of transactions reached the highest record of JPY 11.4 trillion in 2022, a significant decrease of 31.6% compared to 2021. Notably, the large-size overseas deals experienced stagnation, and no deals exceeded JPY 1 trillion, however, other various factors can also be a reason for the decreasing price. Still, it is safe to assume the primary reason was the significant 51.7% decrease in “IN-OUT” deals, which can be attributed to the increased uncertainty due to the ongoing Russian-Ukraine conflict and the depreciation of the Japanese Yen (JPY).

Then, the decrease in “OUT-IN” deals can also represent increased uncertainty in the future. At the same time, considering the number of transactions had increased and the total price of the deals accounted for only a handful of major cross-border deals, it is justifiable that such a large decrease because of the lack of major cross-border deals. Besides that, since the term “M&A” is widely accepted globally, it is reasonable to believe that its importance in corporate management is expected to increase but not decrease.

However, it is concerning that the following issues might take away the vitality of Japan in the mid-to-long term and then decrease the “IN-OUT” deals gradually.

For example, conservative policy and depreciation of vitality due to population ageing; the decrease of consumption due to the depreciation of the JPY and the stock price rise; slow progress of digitalization and conquest of COVID-19, which can probably be one of the byproducts of population aging; the passive management style because of overly gathered attentions to failures of the past major M&A deals; too cautious decision-making of the corporate management due to mindset to avoid any risks and any failures.

Though this is a scenario that many don’t want. Yet, there are possibilities that “OUT-IN” deals will increase, as many are assessing Japanese companies as a relatively reasonable option because of the decrease of their value.